March 23, 2026

The Week Ahead

Markets are being led by geopolitics, with Middle East developments continuing to overshadow fundamentals.

- Markets continue to be driven by conflict in the Middle East, with geopolitical developments remaining front and center. After a volatile weekend, reports that President Trump postponed potential strikes by five days provided some temporary relief. Discussions with Iran remain ongoing, with the risk of disruptions to global energy flows still a key concern.

- The U.S. and China also delayed their planned meeting by five weeks due to the conflict. Markets were highly volatile last week and will likely continue to trade on headlines, with oil, inflation expectations, and broader geopolitical uncertainty outweighing traditional fundamentals in the near term.

- More broadly, macro developments will continue to set the tone across commodity markets. As we saw last week, energy prices and fund flows are driving sentiment across commodities. While the upcoming week is relatively light on major economic data, attention will begin to shift toward next week’s USDA Prospective Plantings report on the ag side.

Market Recap

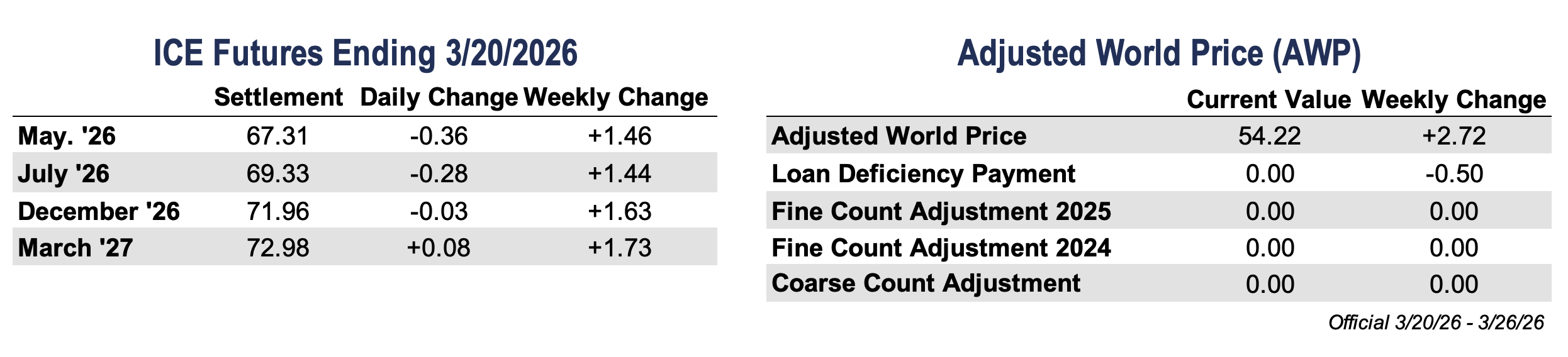

- Cotton futures pushed higher early in the week before giving back some gains into Friday, ultimately finishing modestly higher overall. May futures settled at 67.31 cents per pound, up 146 points on the week, after reaching their highest levels since July 2025 and briefly breaking above the 200-day moving average.

- Strong early-week momentum was driven by heavy fund buying, improved technicals, and supportive headlines, including additional Chinese import quotas and broader commodity strength. As the week progressed, markets shifted into a more cautious tone. Ongoing geopolitical tensions in the Middle East, rising energy prices, and a more hawkish Fed outlook weighed on broader sentiment, leading to some consolidation and risk-off trade across markets. Overall, the market showed resilience despite increased macro uncertainty, but remains sensitive to shifts in demand, geopolitical developments, broader financial market trends, and increasingly concerning drought conditions across the U.S. cotton belt ahead of planting.

- On-call activity continued to improve, with the imbalance between unfixed sales and purchases narrowing for the fifth consecutive week, while record fund buying helped reduce the overall speculator net short position. At the same time, strong prices triggered significant loan redemption activity, with an estimated 2.4 million bales removed from the loan during the week.

- Trading activity was exceptionally strong early in the week before easing into Friday. Open interest decreased 5,171 contracts to 329,146, while volume tapered off to close out the week as the market consolidated following early gains. Certificated stocks decreased 1,149 bales to 115,640.

Economic and Policy Outlook

- President Trump postponed planned strikes on Iranian energy infrastructure for five days, citing ongoing talks aimed at easing tensions. This follows a weekend escalation where he issued a 48-hour ultimatum for Iran to reopen the Strait of Hormuz and threatened to strike major power plants, sending oil above $112 and pushing global yields higher. While Iran has disputed the existence of direct communication, the delay in action briefly pressured oil prices lower after the rally. Looking ahead, markets will remain highly sensitive to headlines, with energy-driven inflation and any progress – or breakdown – in negotiations likely to drive price direction.

- The conflict with Iran is likely pushing any Trump–Xi meeting further out, which is now set to take place in five to six weeks, as U.S. focus shifts toward energy markets and regional security, keeping geopolitics in control of market direction. That leaves tensions elevated and delays any near-term reset, with energy and headline risk continuing to drive sentiment. With heavy export dependence and exposure to China, uncertainty has already kept Chinese buying on the sidelines this year, and any broader slowdown in trade flows or global apparel demand could add pressure to prices.

- Last week, the Fed left rates unchanged at 3.50–3.75% as it navigates the uncertainty from the Iran conflict, particularly the impact higher energy prices could have on inflation. Officials raised their inflation outlook, and markets have turned more cautious, with rate cut expectations fading and hike probabilities increasing. While the war adds another layer of uncertainty, the Fed is largely looking through the near-term oil shock for now. Looking ahead, the path forward will depend on how energy prices and inflation trends develop, leaving the Fed in a wait-and-see mode as geopolitical risks remain elevated.

Supply and Demand Overview

- U.S. export sales softened from the previous week for the period ending March 12. Net upland sales came in at 196,700 bales, down 22% week over week, with Vietnam, Turkey, and India leading the buying. There were 22,000 bales in cancellations from Pakistan and 6,200 bales from Korea, though those volumes were rolled into the 2026/27 crop year, which saw net sales of 122,200 bales.

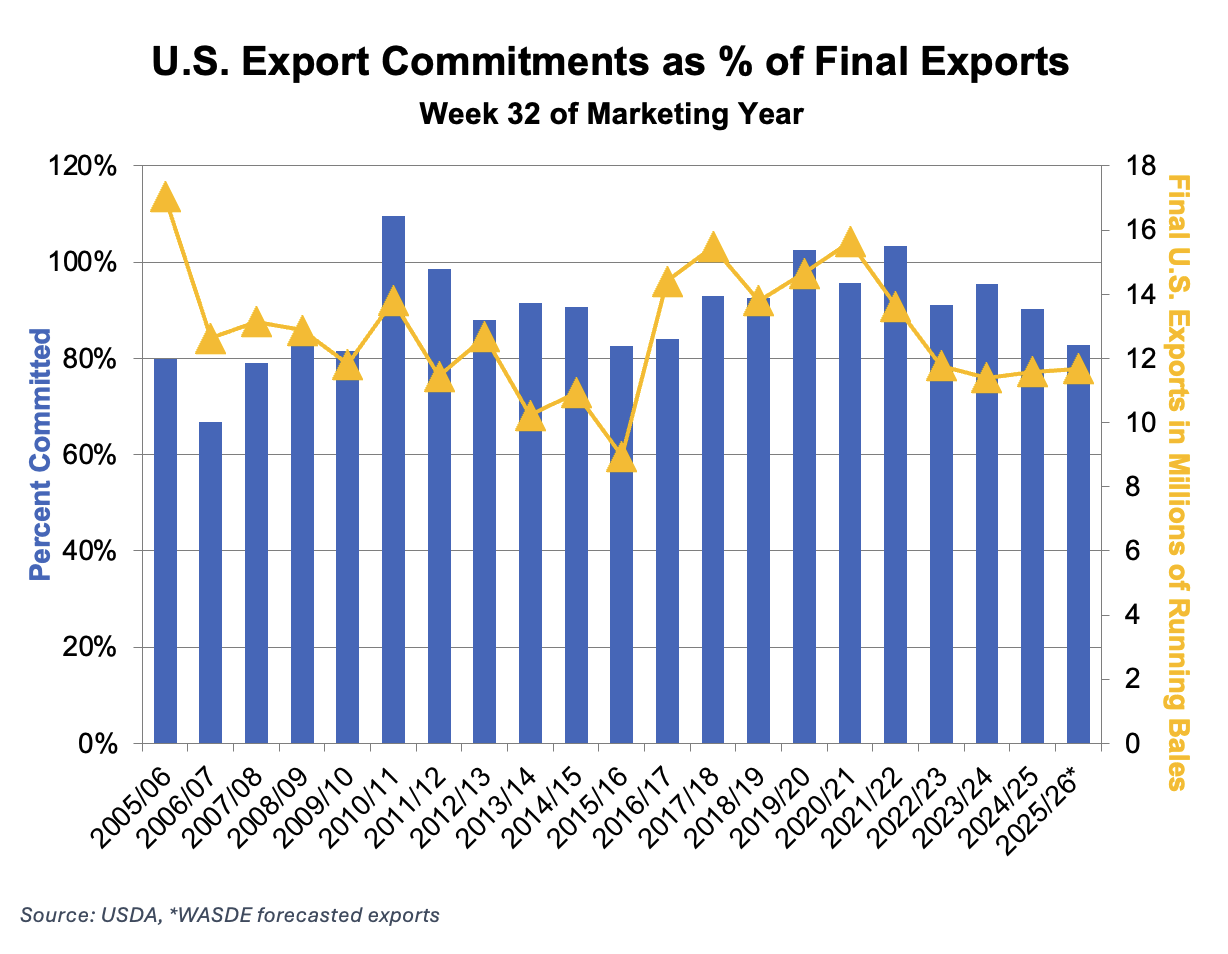

- Shipments totaled 273,900 bales, an improvement from recent weeks but still running below the roughly 300,000 bales per week needed to reach USDA’s 12 million bale export projection. Pima sales increased to 7,800 bales on the week, while shipments edged slightly lower to 5,200 bales.

The Seam®

- As of Friday afternoon, grower offers totaled 20,584 bales. The past week 21,363 bales traded on the G2B platform received an average price of 63.40 cents per pound. The average loan redemption rate (LRR) was 51.68, bringing the average premium over the LRR to 11.72 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).

Sustainability Enrollment Opportunities

- Enrollment for the U.S. Cotton Trust Protocol will be open January 5th- April 30th, 2026. Growers who are currently enrolled will need to renew their membership to continue their involvement in the program. If your gin would like to host an Enrollment Field Day during this time, please reach out to PCCA at (806) 763-8011. Click here for a list of in-person sign-up dates.

- New Grower Enrollment for the Better Cotton Initiative will be open from March 3 to May 30. Growers interested in joining this global sustainability program should contact PCCA (806) 763-8011.