August 3, 2026

The Week Ahead

Cotton heads into the week with crop conditions, export demand, and next week’s August supply and demand report in focus, while Friday’s U.S. employment report highlights the week’s macro calendar.

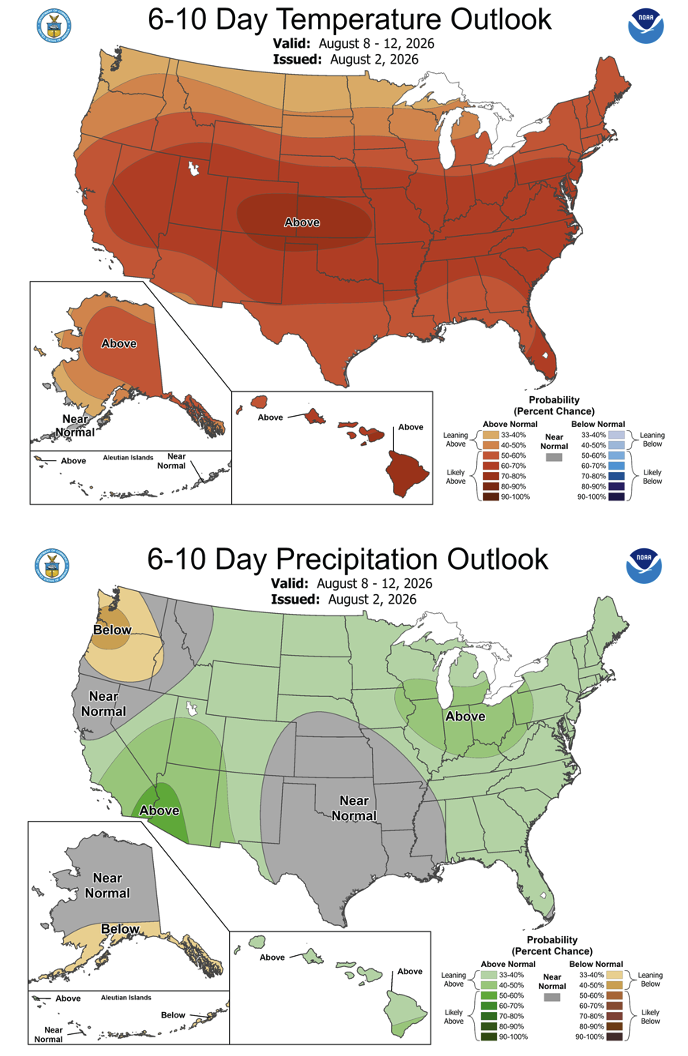

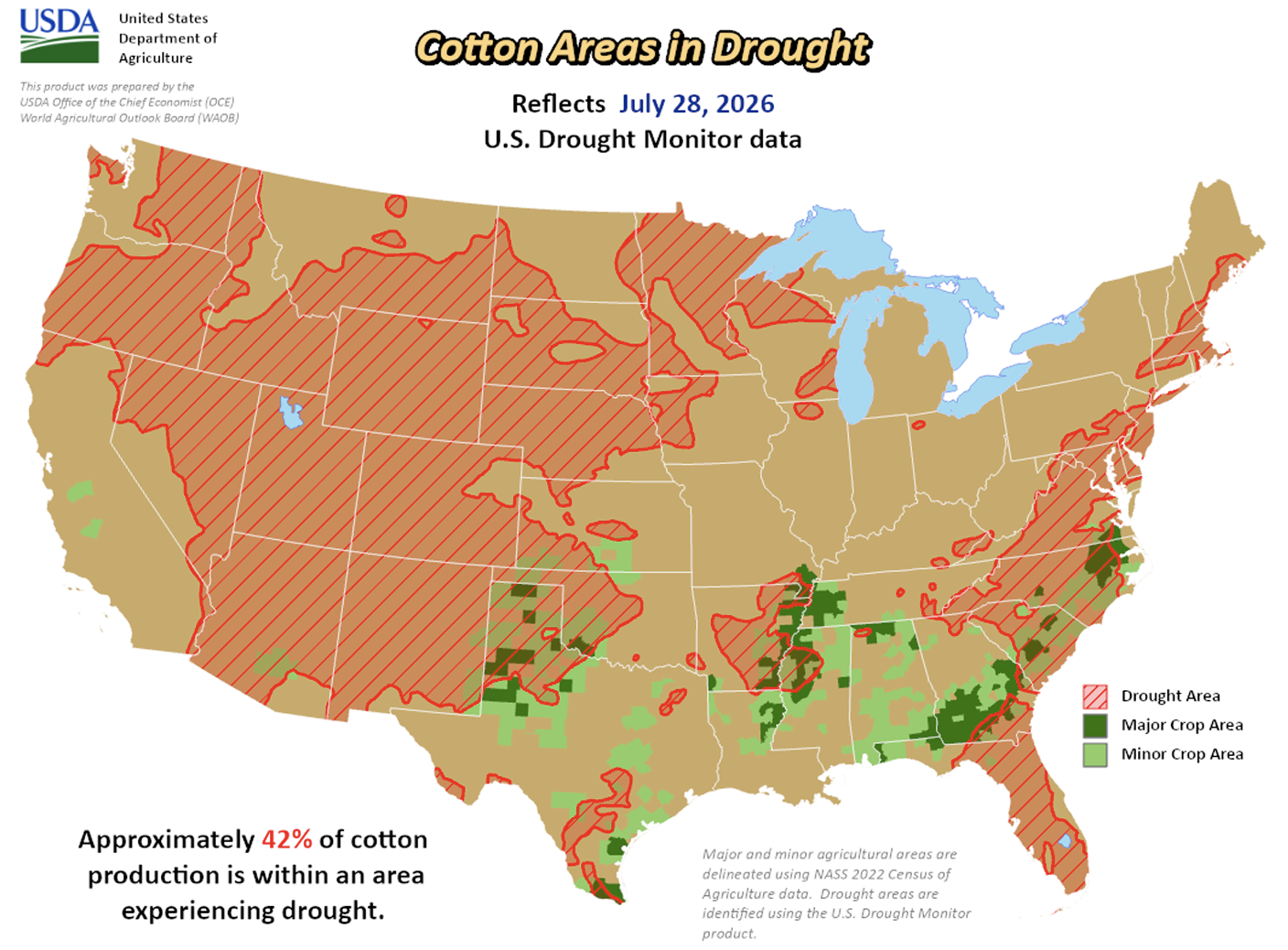

- Crop conditions will remain front and center as the U.S. crop moves through a critical stage of development. Rainfall across portions of West Texas and Oklahoma offered some relief from last week’s intense heat, but coverage was uneven, and hotter weather is expected to return across the Southwest. Monday’s Crop Progress report will provide another update on crop ratings as traders gauge whether recent rainfall was enough to stabilize yield potential.

- Thursday’s Export Sales Report will provide one of the final snapshots of old-crop demand. With only one reporting week remaining after this week’s release before the 2025/26 books close, the report should offer a much clearer picture of where export sales and shipments will finish. Traders will also be watching to see if new-crop commitments build on the solid demand seen in recent weeks.

- Markets will also begin looking ahead to next Wednesday’s August USDA supply & demand report. The August report is one of the year’s most anticipated releases, incorporating certified acreage following the July 15 certification deadline along with updated production estimates based on growing season conditions. Traders will likely begin positioning ahead of the report as the week progresses.

- Friday’s U.S. employment report will be the week’s biggest macro release. A stronger-than-expected labor report could reinforce expectations that interest rates stay elevated, supporting the U.S. dollar and creating another headwind for commodities.

- Markets will also monitor renewed U.S.-Iran talks after hopes for an agreement and the possible reopening of the Strait of Hormuz pushed crude oil sharply lower to begin the week.

Market Recap

- Cotton finished the week higher, with December futures settling at 81.79 cents per pound, up 181 points on the week. Trading was relatively quiet through midweek as the market worked through the Federal Reserve meeting and waited for fresh export data. Buying picked up late in the week as stronger-than-expected export sales, another week of Chinese reserve auctions selling out and reinforcing signs of steady demand, ongoing weather uncertainty, and a weaker U.S. dollar helped lift prices.

- Even with Friday’s rally, December futures once again struggled to push through resistance near 82 cents, leaving cotton within the same trading range it has traded in for several weeks. Trading volume also remained relatively light, suggesting the market is still looking for a larger catalyst before making a more decisive move.

- Weather remained a problem. Prolonged heat across West Texas and Oklahoma kept production concerns elevated through much of the week before rainfall reached portions of the region over the weekend. While the moisture was welcome, coverage was uneven, and traders will now be watching to see how much benefit those rains provide.

- As harvest gets underway in South Texas, much of the High Plains and Oklahoma crop is entering a critical stage of development. Additional August rainfall will be especially important for dryland acres after weeks of triple-digit temperatures, and the next couple of weeks could go a long way toward determining final yield potential.

- Friday’s Commitments of Traders report showed managed money trimming its net long position slightly, while index funds continued adding to their long positions. Overall fund positioning remains supportive, though the market will likely need a stronger weather or macro catalyst to break out of its recent range.

Economic and Policy Outlook

Economic and Policy Outlook

- The Federal Reserve left interest rates unchanged at 3.50% to 3.75%, though three officials favored a rate hike and Chairman Kevin Warsh maintained a hawkish stance on inflation. Economic data sent mixed signals, with second-quarter GDP missing expectations and June core PCE rising less than forecast, though inflation remains well above the Fed’s 2% target, and underlying consumer spending stayed resilient. Sensing a lack of effort from the Fed, some bond traders sold off longer maturities. For cotton, the market is balancing signs of a slowing economy against expectations that interest rates stay higher for longer, a backdrop that supports the U.S. dollar and weighs on commodity prices.

- The Japanese yen rallied after Japan and the U.S. coordinated currency intervention for the first time in 15 years to counter the currency’s prolonged weakness. Because Japan holds significant positions in U.S. Treasuries and plays a central role in global financial markets, further intervention or Bank of Japan policy changes could have broader implications for currencies, bond yields, and investor sentiment.

- WTI crude oil climbed back into the mid-$80s per barrel as renewed tensions between the U.S. and Iran raised concerns over potential disruptions to shipments through the Strait of Hormuz. Although President Trump delayed additional military action to allow negotiations to continue, geopolitical developments are likely to keep energy markets on edge.

- Senate Agriculture Committee Chairman John Boozman released the updated text of the 2026 Farm Bill ahead of this week’s committee markup. The proposal includes roughly $68 billion in additional agricultural investments, $12 billion in supplemental producer assistance, and permanent nationwide year-round E15 sales, though it still faces a difficult path through the Senate. Keep in mind that price supports for cotton and other commodities were enhanced in the One Big Beautiful Bill Act (OBBBA) in July 2025 and, therefore, are unaffected by this portion of the Farm Bill.

Supply and Demand Overview

- The latest Export Sales Report showed Upland sales of 29,700 bales, a marketing-year low, down 42% from the previous week and 41% below the four-week average. Vietnam was the largest buyer, followed by Pakistan, India, China, and Mexico. New-crop sales reached 352,400 bales, one of the strongest combined sales weeks on record, helping support cotton futures late in the week despite weaker old-crop demand.

- Upland exports totaled 233,800 bales, down from the previous week, with Vietnam once again leading shipments, followed by Pakistan, Indonesia, Turkey, and Mexico. With only one reporting week remaining in the 2025/26 marketing year, attention is shifting toward whether U.S. exports will ultimately reach USDA’s 12.2 million bale forecast.

- Pima sales totaled 2,700 bales, led by India, while exports reached 4,500 bales, with nearly all shipments destined for India.

The Seam®

The Seam®

- As of Friday afternoon, grower offers totaled 1,063 bales. The past week, 8 bales traded on the G2B platform received an average price of 57.00 cents per pound. The average loan redemption rate (LRR) was 48.40, bringing the average premium over the LRR to 8.60 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).